)

The market’s rebound from recent turmoil has been so swift it feels quicker than a ray of light. This astonishing velocity leaves investors to wonder: after the lightning, will the thunder follow?

That is the question we aim to explore in our Market at a Glance section. We will unpack the dynamics behind this exceptionally rare rebound and what it means for your portfolio.

In the Demystification Room, we will look beyond the public markets to decode a term gaining traction in investment circles: "semi-liquid." We will explore what it truly means when applied to the world of private credit and why understanding its nuances is crucial.

Finally, we will reintroduce our investment solutions, designed to help you navigate any market with clarity and confidence.

Enjoy the read.

Table of Contents

The market at a glance: Quicker than a ray of light

Song of the month: “Ray of light" by Madonna

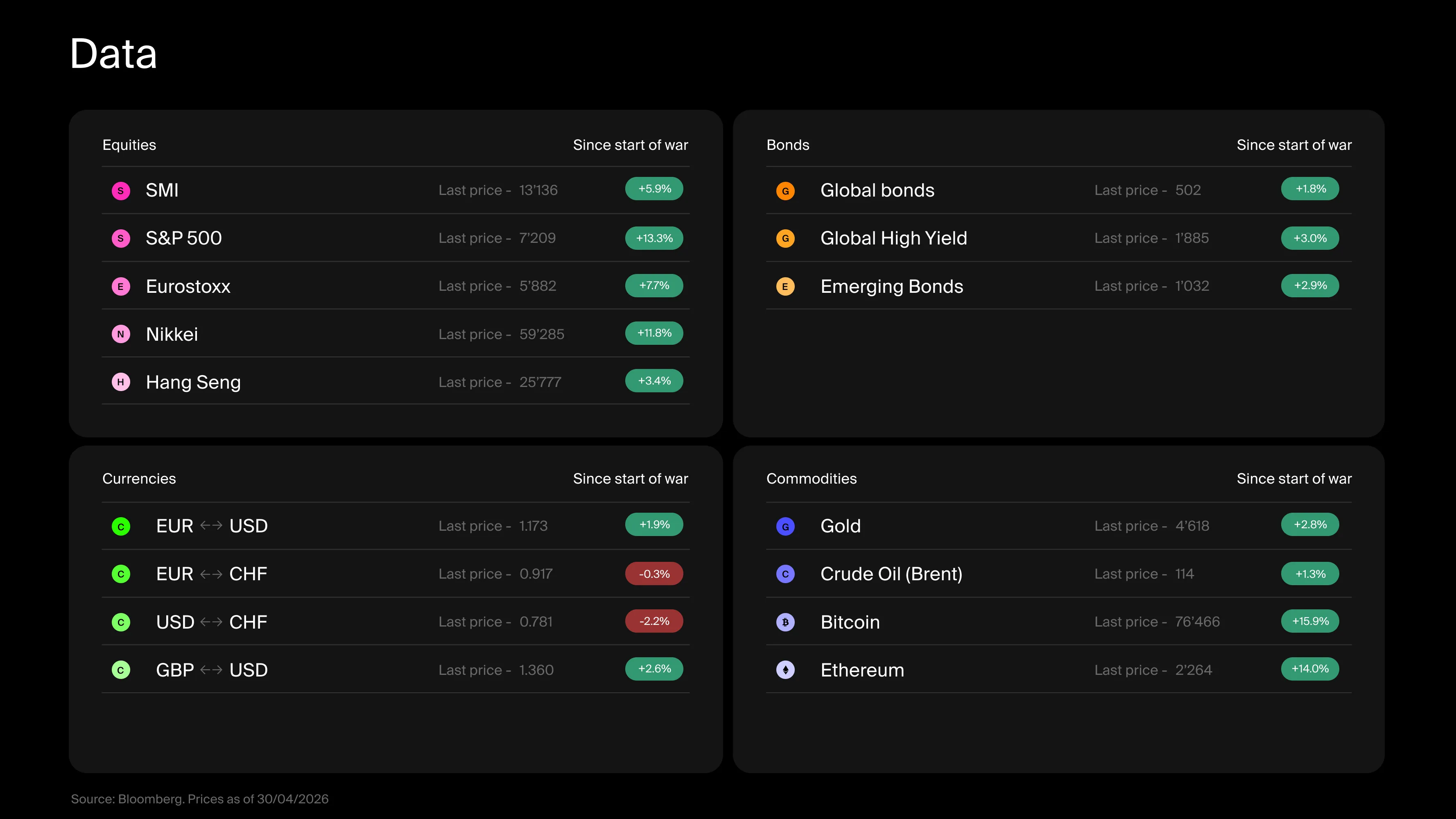

The war in Iran was meant to last a week, now we are heading into the seventh. Markets were expected to remain under pressure as long as the outcome stayed uncertain; instead, they rebounded with astonishing speed. After a relatively modest decline (–9%), considering the potential economic fallout of the conflict, global equity markets surged by more than 10% in just 13 days.

By historical standards, rebounds of such magnitude are exceptionally rare (occurring less than 1% of the time). We are, quite literally, approaching the speed of light.

In that spirit, “Ray of light”, Madonna’s iconic 1990s track, feels like a fitting soundtrack for this monthly note.

All of this leaves us with the question on everyone’s mind: After the lightning, will the thunder follow?

Key takeaways

The war in Iran was expected to last a week; we are already entering the seventh.

Yet equity markets have rebounded at lightning speed, leaving many investors puzzled.

Bond markets have also moved higher, while expectations for the future path of interest rates have been recalibrated.

In commodities, oil remains at the center of attention. Gold is hesitating, while digital assets are attempting to regain momentum.

Although the market downturn was short-lived, it created some compelling dislocations.

What happened with equities

First, a touch of professional humility: few of us anticipated such a rebound, and our team was no exception. Forecasting is not our core discipline, but as firm believers in risk management, we always consider multiple scenarios. A rebound after a downturn is never improbable, but this one stands out for both its speed and its magnitude.

Not that we are complaining. It is always welcome to see portfolios regain momentum. US equities are up 13.3%, pulling most other markets along in their wake, from Europe to Switzerland to China.

However, such a swift return to prior levels puts us in a more delicate position. The downturn was too brief to fully unwind some of the structural excesses that have built up in recent months, while the rebound has been too strong to ignore the persistent upward pressures supporting markets at the slightest sign of weakness.

The macro picture is equally mixed. From investor positioning to the first batch of Q1 2026 earnings, which have been broadly solid (so far, 28% of US companies have reported, with 84% beating expectations) to sustained demand for AI, there is no shortage of reasons to remain constructive in the short term. Yet, with oil still hovering near $100 per barrel, inflationary pressures re-emerging, and negotiations around a ceasefire dragging on, not all signals are pointing in the same direction.

That said, expecting a perfectly clear outlook is akin to wishing markets would never surprise us. It is neither realistic nor desirable and it would strip investing of its very essence. It is precisely when the path forward is uncertain that creativity matters most, and when investors can hope to be rewarded for the risks they take. From introducing downside protection to deploying strategies less dependent on market direction, opportunities remain abundant.

The backdrop is, in fact, quite supportive. The decline in volatility and the dislocations observed across several segments of the market are creating compelling opportunities. Geographically, the anticipated effects of the war have played out unevenly. Since the start of the conflict, across 92 global equity indices, the gap between the best and worst performers has reached 32%. This dispersion could pave the way for attractive catch-up trades, and entry points are still very much present.

What happened with bonds

IDislocations are not confined to equity markets; they are also evident in fixed income. For instance, it is striking that investors are broadly anticipating rate cuts in the United States, while in Switzerland and Europe, expectations are more decisively skewed toward rate hikes.

To some extent, this is encouraging news for Swiss savers, as it pushes back the prospect of a return to negative interest rates, although caution is warranted when drawing firm conclusions.

Against this backdrop, April proved to be broadly supportive for bond markets, which delivered a gain of more than 1.8%.

What happened with commodities, currencies, and digital assets

Some of the divergences observed in rate markets are also reflected in foreign exchange, with tangible implications for Swiss investors. While the Swiss franc weakened against both the dollar and the euro in March, it reversed course and appreciated in April.

In commodities, oil remains the key variable drawing everyone’s attention. It has the potential to shape the course of events, both economic, particularly through its impact on inflation, and geopolitical, by determining which countries are best positioned to cope with a potential supply shock.

It is also worth examining the behavior of gold and digital assets. The former is showing concerning signs of fatigue. As we highlighted last month, gold tends to rally in anticipation of risk, but not necessarily once that risk materialises. After declining in March, it failed to rebound in April, despite what appears, on paper, to be a supportive environment. This may raise doubts among investors, especially those who entered the market late, at record levels.

Digital assets, for their part, are still struggling to recover from their recent correction, while attempting to reassert their value proposition in the current environment. Another potential relative-value trade?

To conclude, while neither economic data nor headline news inspire full confidence, and the risk of a correction remains, the opportunity set has arguably never been broader. We therefore remain constructive. The question is whether one will need to move faster than a ray of light to seize it!

)

Demystification room: Did you say “Semi-liquid” ?

Private credit has been making headlines with increasing frequency. Over the past two decades, the market has expanded dramatically, growing nearly tenfold to an estimated $3 trillion today. In the aftermath of the 2008 financial crisis, banks were subjected to tighter regulation and became far more selective in their lending. Demand for capital, however, never disappeared. As companies continued to require financing, private funds stepped in, gradually replacing banks as lenders to higher-risk borrowers.

Historically reserved for institutional investors such as pension funds, these strategies have recently been opened to a broader audience, including private investors. The pitch is compelling: higher returns, lower apparent volatility, and, perhaps most importantly, access conditions portrayed as flexible.

This is where the notion of “semi-liquid” comes into play. In essence, these are funds that promise investors the ability to redeem their capital at regular intervals (quarterly or semi-annually) for example. However, this promise rests on a fragile assumption: that the underlying assets can be sold without difficulty if needed.

In reality, the loans held by these funds are inherently illiquid. They are not traded on open markets, and finding a buyer can take time, particularly in periods of stress. As long as only a limited number of investors request redemptions, the system functions smoothly. But if many investors seek to exit simultaneously, the fund faces a simple constraint: it cannot sell assets quickly without accepting a discount, or it must restrict withdrawals.

Ultimately, the term “semi-liquid” can create a misleading sense of security. In practice, an asset is either liquid, or it is not.

Clarity for your portfolio in uncertain markets

It is precisely in such moments of dislocation that your portfolio needs clarity when markets don't have any. At Alpian, you get expert but accessible investing solution, letting you navigate any market with confidence. We’ve recently renamed our investment plans and are taking this opportunity to reintroduce them to you:

Managed Essentials: An easy-to-use ETF-based discretionary portfolio starting from just CHF 2'000, with four distinct portfolios and five risk profiles.

Managed Premium: A fully personalised discretionary portfolio from CHF 30'000, continuously optimised by our experts.

Guided Premium: A highly personalised advisory portfolio starting from CHF 10'000, ideal for proactive investors.

History shows that staying invested in a diversified portfolio can help building long-term wealth.

Disclaimer : Investments involve risks, including the possible loss of invested capital. The value of investments can fluctuate and there is no guarantee of making profits or avoiding losses. Diversification does not ensure a profit or protect against a loss. Potential investors should consult a qualified financial advisor before making any investment decisions. Please read the full risk warnings and other relevant documents on our website before investing.

)

)