)

There are moments when market analysis feels almost secondary to the events driving it. We are living through one of them. A new conflict has emerged, volatility has resurfaced, and once again markets are being forced to react to developments far beyond economic fundamentals.

History suggests that markets eventually learn to look through wars, even as the human cost endures far longer. But it is far too early to conclude that the adjustment is complete, however modest our discomfort as investors may be when compared with the suffering thousands of civilians will endure. Markets may move on, but the path there is rarely linear or predictable.

As outlined in our Demystification Room, Iran occupies a critical geopolitical crossroads, and tensions in the region can propagate swiftly, with broader economic consequences. In such an environment, we must remain focused and, while we wait for a better world, continue to design more resilient portfolios.

Table of Contents

The market at a glance: Imagine

Song of the month: “Imagine" by John Lennon

As we were already marking, in February, a rather inglorious anniversary, the Ukraine conflict entering its fifth year, a new theater of war has ignited in the Middle East, a conflict long feared both for its own sake and for the spillover effects it could unleash. This weekend, the United States and Israel carried out strikes on Tehran, killing several Iranian leaders, and retaliation was swift. Since 2009, the number of armed conflicts worldwide has nearly doubled. Should this trend persist, 2026 will become yet another data point in an increasingly troubling trajectory.

In this context, it felt inappropriate to select an original soundtrack for this commentary. Instead, Imagine by John Lennon seemed more fitting, in the hope that its timeless message might, if only briefly, temper the world’s rising belligerence.

Key takeaways

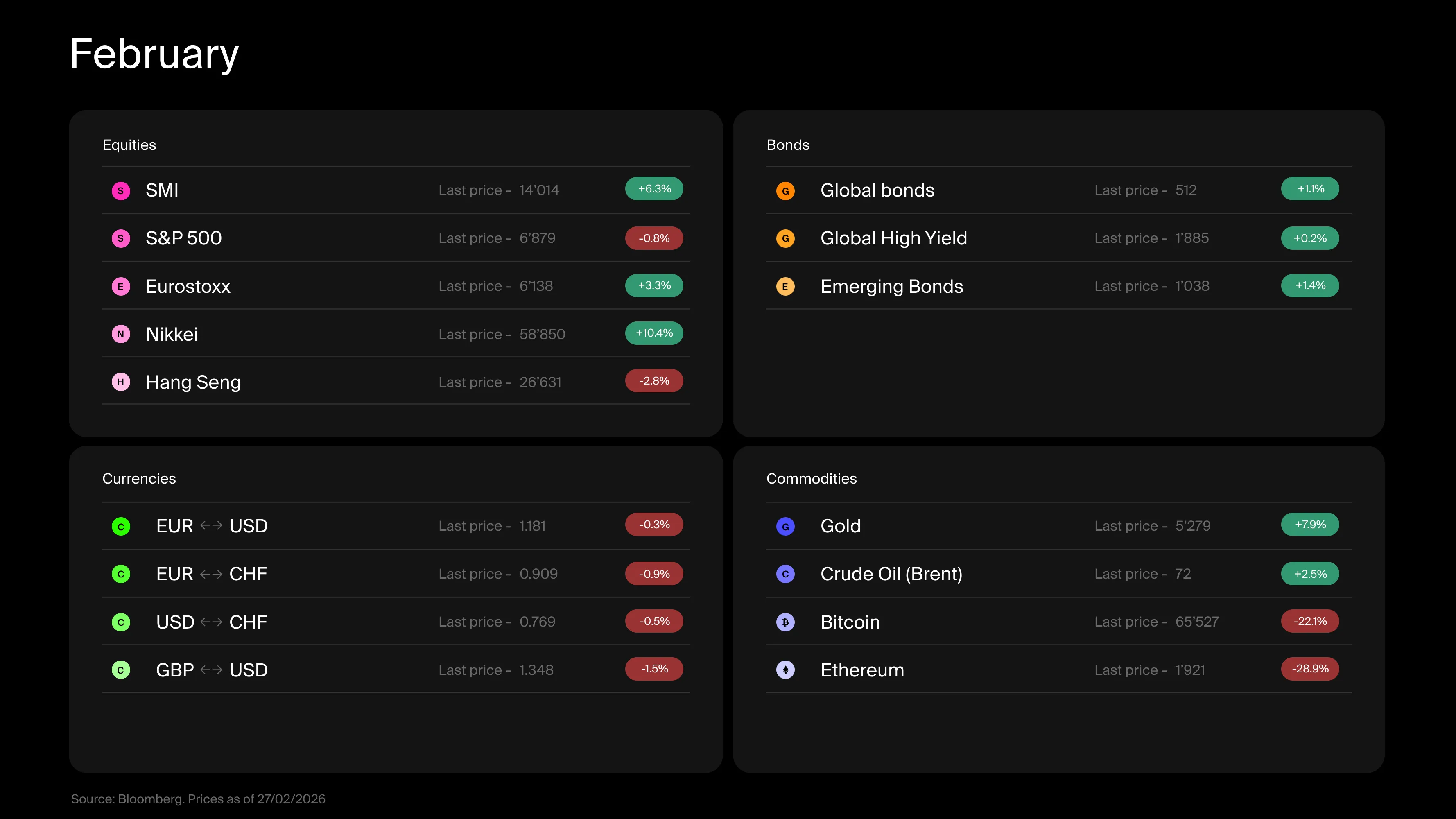

After a relatively strong month of February, markets reacted sharply to developments in Iran.

Nervousness had already been building in equity markets in recent weeks, and the announcement of renewed conflict accelerated profit‑taking.

Bond markets, which had benefited from easing inflation expectations, may face renewed pressure if oil prices continue to rise, potentially leading to higher interest rates.

The most pronounced reaction was observed in commodity markets.

This shock has also helped clarify which assets truly deserve their safe‑haven status: gold has responded as expected, while cryptocurrencies have disappointed.

At this stage, it remains difficult to assess whether the impact of these events will be lasting, but a period of market turbulence appears likely.

What happened with equities

In February, global equity markets ended the month in positive territory, though signs of unease were already visible even before events in Iran. The Swiss market posted a strong gain of 6.3%, while European, Japanese, and emerging markets also performed well.

This stands in contrast to the markets of the major superpowers, which are struggling to regain momentum. In the United States, the benchmark equity index has effectively moved sideways for the past three months, and investor fatigue toward Chinese markets is increasingly evident. This regional divergence is noteworthy: it signals not a broad disengagement from risk, but rather a selective reallocation.

Since Donald Trump’s return to the White House, investors have experienced no shortage of emotions. Over time, however, the political noise has become structural, and the long‑term strategy of the U.S. administration has grown clearer. Aggressive fiscal stimulus and a more protectionist stance, supported by measures of varying ingenuity such as tariffs and digital‑asset regulation, aim to finance the transition while preserving confidence in the U.S. dollar system.

This sense of direction, combined with equity returns boosted by artificial intelligence, allowed investors to settle into a rhythm. Internationally, markets had begun to accept the idea of a changing “global order,” a theme that dominated discussions in Davos.

That fragile equilibrium was disrupted in February. First, the U.S. Supreme Court invalidated so‑called reciprocal tariffs, followed by President Trump’s decision to introduce a 10% global tariff. For some, this was a relief; for others, a disappointment. For all investors, however, it introduced a new variable with complex implications.

A second realization also emerged: the promises of artificial intelligence are themselves volatile. Massive investment flows and extraordinary returns have contributed to a growing cohort of skeptics. A recent example was a report published by the research firm Citrini, whose alarmist tone reportedly triggered market declines.

That a report from a firm previously unknown to the general public could unsettle Wall Street says less about the report itself than about a mature market increasingly driven by narratives rather than data. Still, credit where it is due: Citrini executed a notable publicity coup.

Finally, President Trump’s reversal on his pledge not to initiate new conflicts in the Middle East has left investors uneasy, though their discomfort pales in comparison to the suffering of the thousands of civilians who will bear the true cost of war.

At this stage, it remains difficult to fully assess the market impact. Markets reacted sharply to the news, as expected. Historically, after an initial sell‑off, markets tend to become relatively indifferent to armed conflicts, particularly when they occur at a distance and supply chains can be adjusted quickly.

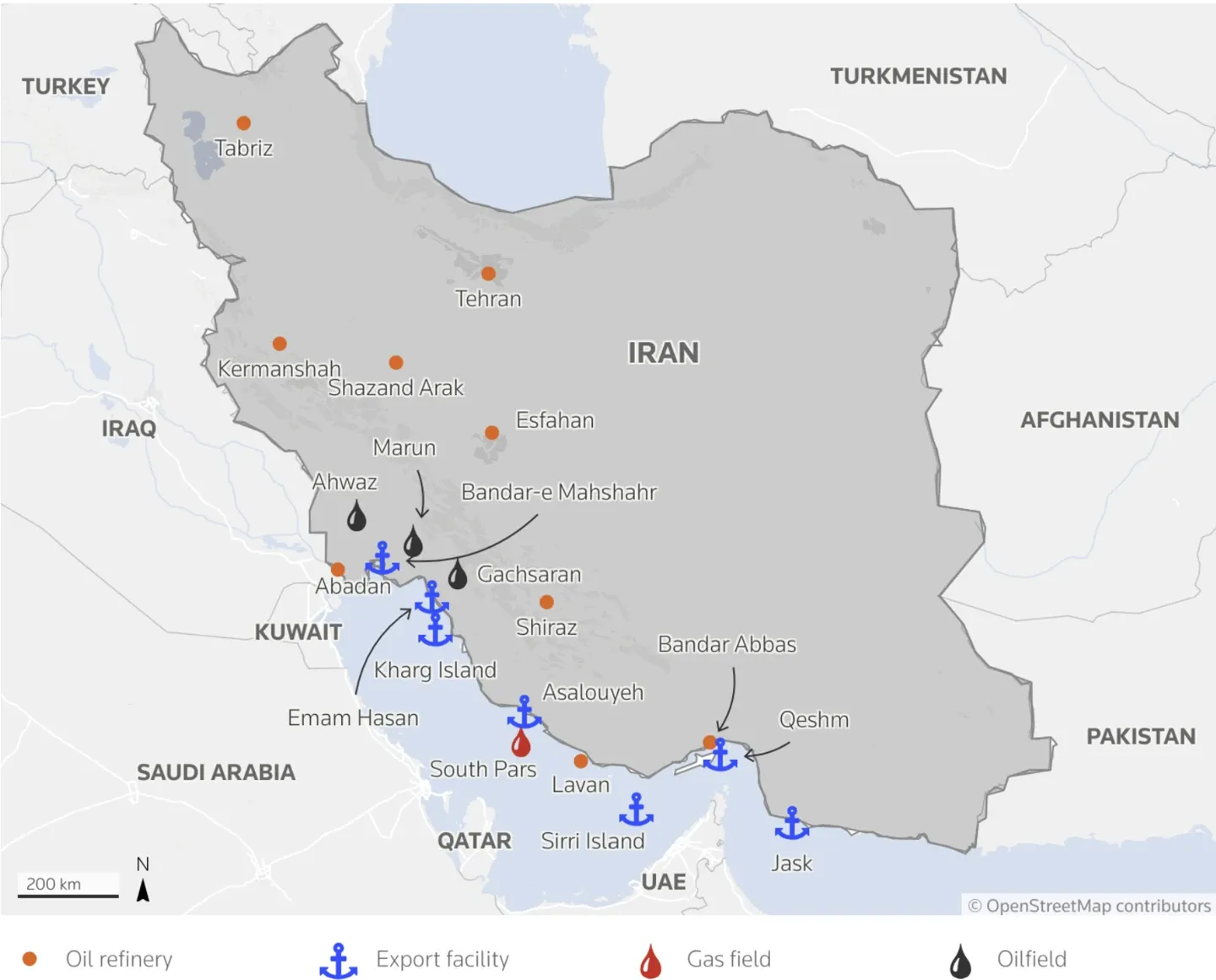

That said, as discussed earlier, Iran represents a uniquely complex geopolitical node: seven land borders, a strategically vital maritime presence along the Strait of Hormuz, and well‑established networks of indirect regional influence. In such a context, a conflict that appears limited can rapidly turn into a powder keg (see demystification room section)

What happened with bonds

For several weeks now, and independently of this latest conflict, investors have been displaying heightened risk aversion, a trend also reflected in bond markets, which ended the month higher.

In February, interest rates declined markedly. This move reflects market expectations of slowing economic growth and moderating inflation. In simple terms, investors believe the economy may lose some momentum, making bonds more attractive.

However, this scenario remains fragile. If commodity prices, particularly energy and agricultural goods, were to rise sharply and persistently, inflationary pressures would likely re‑emerge. Sustained commodity inflation could force central banks to keep rates higher for longer, or even raise them again, with negative implications for both bond markets and portfolios.

What happened with commodities, currencies, and digital assets

While equity and bond markets reacted to events in Iran, the strongest tensions were felt in commodity markets, as expected. Oil prices surged, nearly 20% of global oil supply passes through the Strait of Hormuz, while safe‑haven assets, led by gold, attracted anxious investors. This is not without risk, however, as gold is already trading at historically elevated levels.

The Swiss franc, which had appreciated significantly since the beginning of the year, has paused. Cryptocurrencies, meanwhile, appear once again to fail the test of safe‑haven status, a role they have long claimed.

To conclude, a period of turbulence should be expected. Market consolidation phases are never comfortable, but they do offer one advantage: should markets correct, this period will provide valuable insight into which diversification strategies truly work and which assets investors turn to when conditions deteriorate.

While we wait for a better world, we can at least design more resilient portfolios. Peace is not a financial variable. But resilience can be modeled.

)

Demystification room: Iran: A Complex Linchpin in the Middle Eastern Balance

Iran is often described as a complex geopolitical linchpin in the Middle East due to the unique combination of its geography, regional power, and strategy of indirect influence. Positioned at the crossroads of the Middle East, Central Asia, and South Asia, the country shares seven land borders with states whose political and security balances are often fragile, multiplying potential points of friction. Added to this is Iran’s strategically vital maritime frontage along the Strait of Hormuz, through which nearly 20% of global oil supply transits, making any tension involving Iran a matter of global energy security.

Beyond geography, Iran projects its influence through a network of regional allies and proxy forces, notably in Lebanon, Syria, Iraq, and Yemen, allowing it to exert power without direct confrontation. This approach makes conflicts more diffuse, harder to contain, and significantly increases the risk of spillover effects. What begins as a localized incident can quickly escalate into a broader regional crisis, disrupting trade routes, driving up energy prices, and drawing in major global powers.

Finally, Iran’s enduring rivalry with the United States and Israel, combined with the unresolved nuclear issue, sustains a climate of chronic mistrust. In this context, Iran acts as a true crisis multiplier: the primary concern is not the initial scale of a conflict, but its capacity to spread, destabilize the wider region, and, by extension, affect global financial markets.

)

Source: LSEG

Tax season just got easier

While geopolitical shocks and market swings may be beyond our control, tax season doesn’t have to be.

Your e-tax statement is now available directly in the Documents section of your Alpian app. In just a few seconds, you can order it and import your complete financial data into your cantonal tax software, skipping manual entry entirely.

The e-tax statement is available for CHF 25.

For Signature members, it is included in your plan at no extra cost.

)

)

)