)

Headlines, ultimatums, sharp market moves…when there’s a lot to unpack, it can be helpful to take a step back and look for precedents in the annals of market history. Today’s environment echoes many episodes from the past century. History may not repeat itself, but it can certainly help us prepare for a range of possible outcomes. That’s precisely what we aim to do in our Market at a Glance section.

In the Demystification Room, we turn to a lighter topic (pun intended), yet one that is no less topical: how weight‑loss drugs are rapidly becoming all the rage among investors. Finally, we’ve invited one of our partners to share insights on the potential implications of the Swiss National Bank’s latest (non-)move on your finances.

Enjoy the read.

Table of Contents

The market at a glance: Back in Time

Song of the month: “Back in Time" by Huey Lewis & The News

This month, I am going to break a rule I had set for myself ever since I started writing market commentaries: never give in to the temptation of using over‑quoted economic clichés.

And yet here I am, about to do exactly that with one I have heard more times than I ever wanted to: “History doesn’t repeat itself, but it rhymes.”

To ease the pain, and in keeping with the spirit of this column, let me serve it with a soundtrack. I invite you to read this alongside Back in Time by Huey Lewis & The News, from the Back to the Future soundtrack (let’s stay on theme). Because yes, we are about to go back in time for a brief exercise in historical versification. If we’re going to look for rhymes in history, we might as well do it properly.

Key takeaways

Since the beginning of the conflict in Iran, market movements have had a distinct sense of historical déjà‑vu.

Equities are down, oil is up, inflation expectations have been revised higher, nothing that could genuinely be described as surprising.

Elsewhere, however, from bond markets to traditional safe havens and even digital assets, the adjustment has been less straightforward.

History may not repeat itself, but it often rhymes. Can it at least give us a few clues about what comes next?

What happened with equities

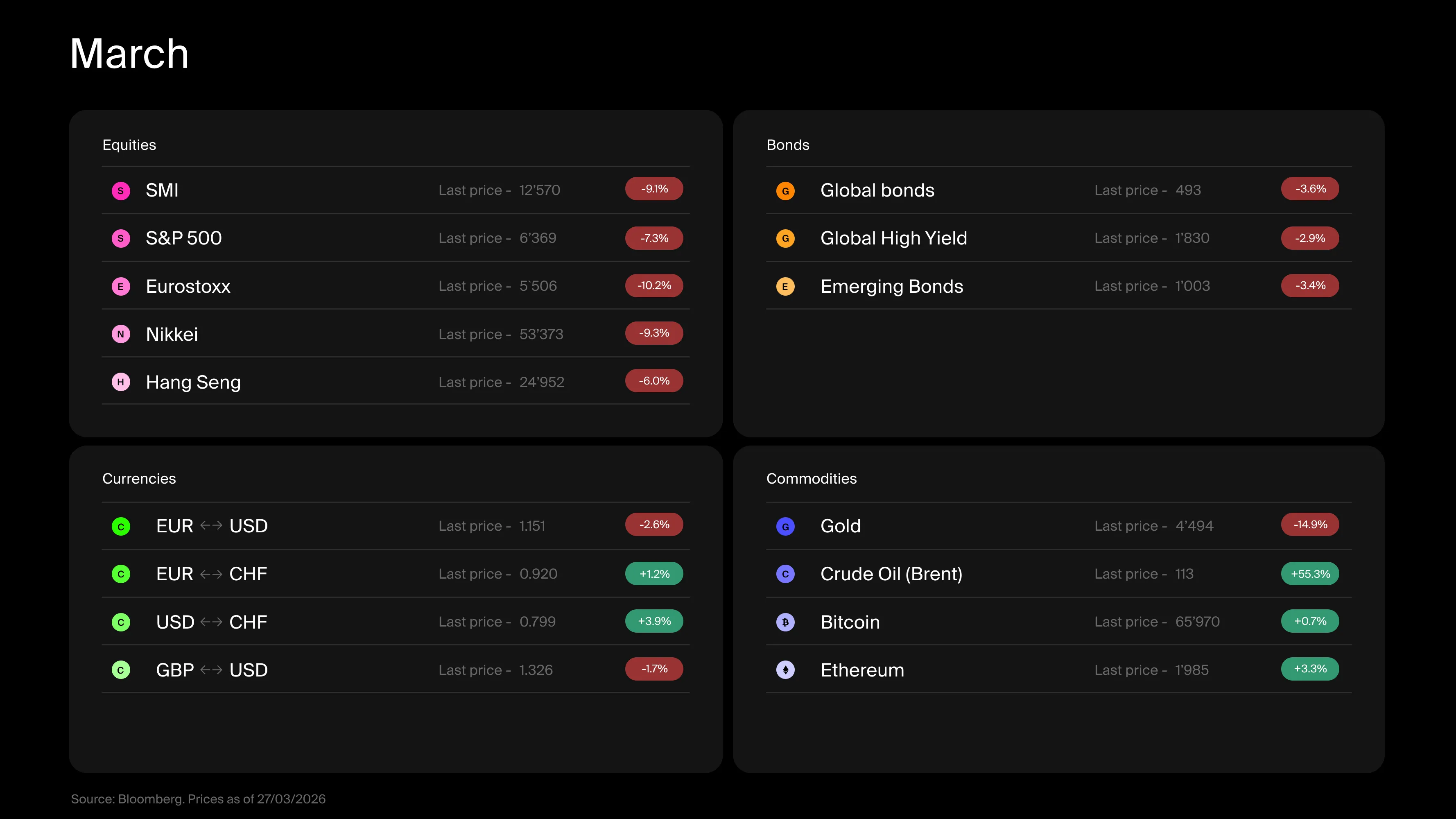

The outbreak of war in Iran on February 27 and the market reaction that followed immediately felt familiar. Equities absorbed the shock: Swiss stocks fell by 9.1% over the month, Europe by 10.2% and the United States by 7.3%. A reaction that appears far from exceptional… at least by historical standards.

If we do find rhymes in economic history, it is not because market outcomes are predetermined, but because investors tend to react in similar ways when confronted with similar environments. From there, it is a short step to talk about cycles, one I am not necessarily willing to take.

In any case, we don’t need to go back very far to find an echo of today’s situation. Just four years ago, Russia invaded Ukraine, and so far the market response looks eerily similar.

In 2022, global equities lost nearly 28% between peak and trough. If there is a rhyme here, it is hardly the work of a great poet.

Looking further back over the last fifty years, there is no shortage of similar episodes. Unfortunately, conflicts in the Middle East are frequent historical reference points: the Yom Kippur war and the 1973 oil embargo, Iraq’s invasion of Kuwait in 1990, the war in Afghanistan followed by the invasion of Iraq…

From an equity market perspective, the pattern is often the same: an initial sell‑off, as investors attempt to assess the economic and financial consequences.

As long as this adjustment phase continues, periods of heightened volatility should be expected.

What happened with bonds

If the reaction in equities was immediate, and broadly consistent with historical precedent, bond markets have struggled to settle on a direction.

Historically, bonds tend to act as a shock absorber when equities fall. But this reflex is highly context‑dependent. In periods of economic slowdown, investors typically rotate toward perceived safe assets. At the same time, central banks loosen policy by cutting rates to support growth, a favourable environment for bonds.

The situation is quite different when the shock originates from rising commodity prices.

If energy costs surge and inflation risks re‑emerge, central banks have less room to manoeuvre. Cutting rates in such an environment risks fuelling inflation further.

From this perspective, today’s backdrop bears greater resemblance to past oil‑driven episodes, such as 1973, 1990 or more recently 2022, than to crises such as 2001–2003.

This poses a real challenge for portfolios relying heavily on the traditional negative correlation between equities and bonds.

What happened with commodities, currencies, and digital assets

On the commodities side, the sharp rise in oil prices surprised no one. It is a near‑constant feature across comparable historical episodes.

Gold and the Swiss franc, traditionally perceived as safe havens, have, however, declined. Is that really unexpected?

Not quite. Contrary to popular belief, gold tends to rise when geopolitical risks increase, but less so when they actually materialise. Similarly, the Swiss franc historically appreciates more during periods of latent uncertainty than amid full‑blown turbulence.

As for digital assets, the recent cooling in investor interest may have spared them from the worst, though for the title of ultimate safe haven, they will have to wait their turn.

What should we take from this exercise?

First, similar causes often produce comparable effects. Expecting a swift return to calm may be optimistic.

Second, differences across crises are largely driven by context. During the first weeks, markets focus primarily on the conflict’s immediate impact, and on the potential resurgence of inflation. The next stage will revolve around growth prospects and the robustness of the economic foundations supporting them. For now, fundamentals remain resilient. But with exuberance still evident in AI‑related equities and cracks appearing in parts of the private markets, vigilance is warranted, particularly as retail investors show signs of fatigue after months of reliably buying every dip.

Finally, past episodes serve as a useful reminder of the true diversifying power of certain asset classes. Choosing the right hedges matters.

Sometimes, the best strategy is to expect the worst, and prepare your shopping list when it arrives. This time, poetry will have to wait

)

Demystification room: The first weight‑loss drug that might move GDP?

GLP‑1 drugs like Ozempic and Wegovy were meant to treat diabetes. Instead, they may end up treating macroeconomists with insomnia. By suppressing appetite, they reduce calorie intake by roughly 20–30% per day, which explains why many now see them as a magical recipe to stay slim. Adoption in Switzerland remains modest: weight‑loss injectables such as Wegovy only became commercially available in late 2023, well after approval, and access remains constrained by high prices and limited insurance coverage. In other parts of the world, however, demand has surged, with prescriptions for GLP‑1 drugs rising by nearly 587% since 2019 and usage among non‑diabetic patients exploding even faster.

And this is exactly the kind of story markets love, because investors can let their imagination run wild. Imagine a drug powerful enough to affect some of our behaviours in a profound way: what we eat and drink, our productivity, our need to go to the gym, the size of the clothes we buy or even how much weight planes have to carry. Suddenly, you can start speculating about the implications across entire sectors. Would Nestlé need to rethink its strategy if millions of people consume fewer snacks? Will airlines burn less fuel if passengers gradually slim down? Could alcohol demand weaken if cravings fall? Of course, much of this narrative is likely exuberant but it illustrates how a medical breakthrough can quickly morph into an economic storyline.

Source: The GLP-1 trend: What the real-world data reveals

SNB: The 0.00% rate reassures... but the real signal is elsewhere

Article written in collaboration with PLUS, Swiss expert in accounting, taxation, insurance and mortgages.

The SNB's decision to maintain the key interest rate at 0.00% announced on March 19, 2026 may at first glance be read as a signal of continuity. For the Swiss real estate market, this decision remains rather reassuring: it supports favorable mortgage financing conditions and limits fluctuations in mortgage rates at this stage. But this does not mean that rates will remain low for long. It is above all a decision to buy time in a context that is becoming more uncertain.

The SNB's real message is more nuanced...

)

)

)