)

With the G7 summit in the headlines and central banks raising their voices, it feels like the adults are back in charge this month. But as we explore in our Market at a Glance, equity markets are only half listening, preferring to chase the latest shiny trends while policymakers try to keep things in order.

In the Demystification room, we step back from the macroeconomic noise to tackle a fundamental question: where does your money actually go when you invest? Spoiler alert: most of the time, it isn't going where you think.

Finally, we partner with the experts at PLUS to unpack the Swiss National Bank’s latest decision to hold rates at 0.00% and what this quiet status quo means for your mortgages and investments.

Enjoy the read.

Table of Contents

The market at a glance: The adults are talking

Song of the month: «The adults are talking» by The strokes

As temperatures rise and summer settles in, Geneva is slowly emerging from its post‑G7 lull. Shops are reopening, football fans are filling bars, and children are flocking to swimming pools. The adults have spoken, life can resume. And to mark the occasion, I borrow from The Strokes’ track: «The adults are talking.»

While some were protesting and taxpayers were footing the bill, the adults were indeed talking. About what exactly? That, we may never fully know. At this year’s G7, amid surprise guests, bold statements and a race for selfies, world leaders tackled major strategic issues: armed conflicts, critical mineral dependencies, macroeconomic imbalances, and the rise of artificial intelligence. Plenty of buzz, few concrete decisions but at least the announcement of a potential agreement between the United States and Iran. If letting the adults talk helps save lives, we’re happy to stay in our room.

Key takeaways

G7, a potential peace deal… in June, the adults are back in charge.

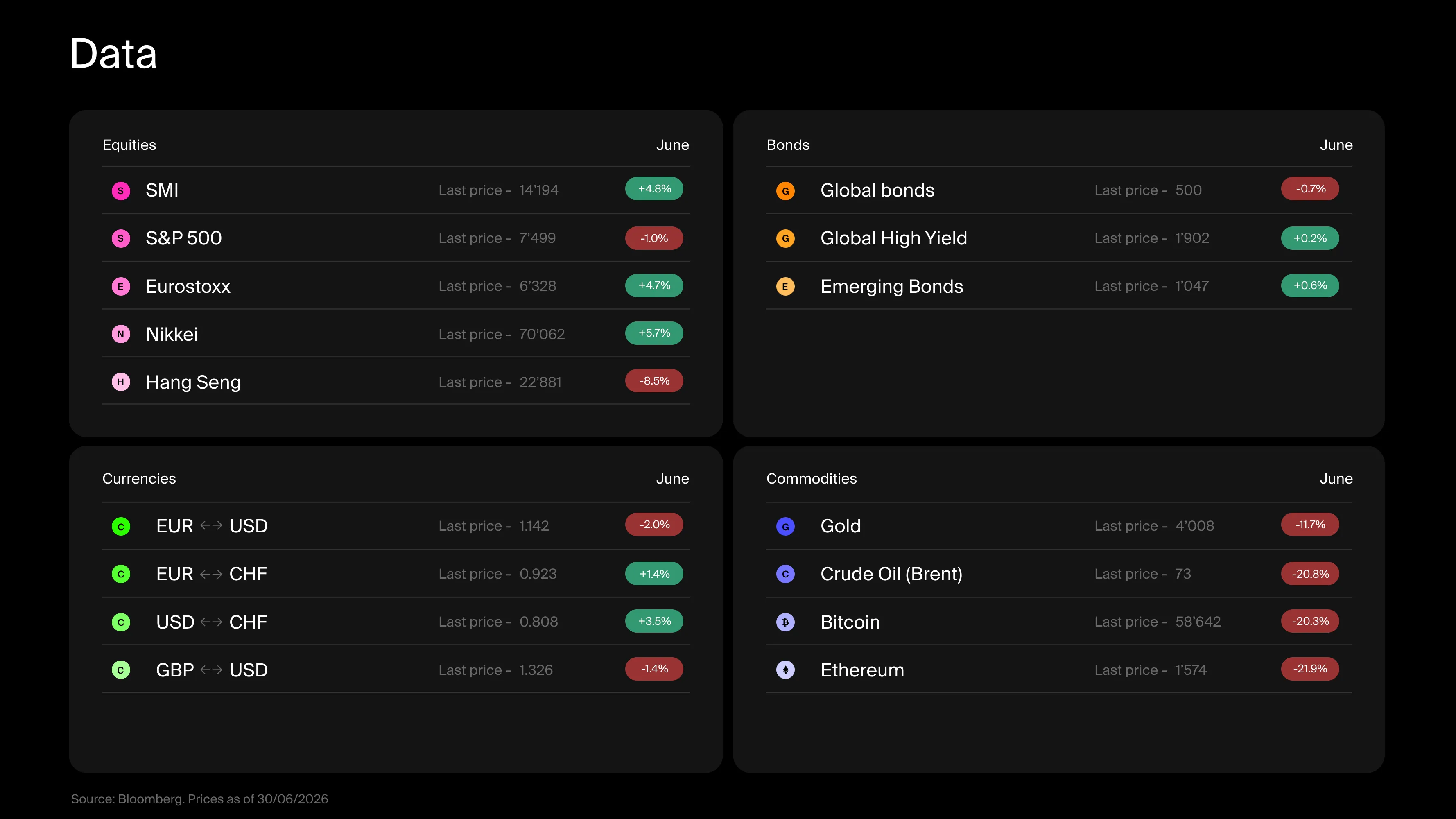

Equity markets, however, are only half listening: choppy performance and an ongoing preference for what shines.

In fixed income, central banks are speaking up again and striking a more hawkish tone.

With the prospect of a U.S. agreement with Iran, oil prices are easing, while gold continues to correct.

In digital assets, cryptocurrencies are starting to feel like a hot potato, with outflows continuing.

What happened with equities

Equity markets barely reacted. Perhaps they were simply too busy with more exciting distractions, like the SpaceX IPO, arguably more compelling than listening to policymakers.

Outside the U.S., most indices posted modest gains since the start of the month, albeit at a sluggish pace. The market remains split in two: on one side, the presumed beneficiaries of AI; on the other, everything else. True to form, investors continue to chase what shines.

The race for the largest market capitalization remains captivating. In just a few weeks, three companies (Micron, SpaceX, and Eli Lilly) joined the exclusive «trillion‑dollar club». It does carry a hint of exuberance, even if several key downside risks have eased.

What happened with bonds

Another «adult» making headlines is Kevin Warsh, the new Chair of the Fed. His appointment has fueled speculation for months, and his first speech signals a clear shift from Jerome Powell’s approach: a willingness to reform the Fed, a renewed focus on price stability, and a different communication style.

For now, bond markets are watching closely, but are increasingly pricing in rate hikes by September.

Across the Atlantic, the European Central Bank has already acted, raising rates by 25 basis points in response to renewed inflationary pressures linked to the Middle East conflict, breaking more than a year of policy inertia.

Meanwhile, the Swiss National Bank is playing for time, prioritizing the strength of the franc over inflation concerns. Not ideal for savers, but at least the era of negative rates now seems firmly behind us.

What happened with commodities, currencies, and digital assets

In commodities, oil remains front and center. The prospect of a durable agreement with Iran has helped ease tensions, bringing prices to around USD 74 per barrel at the time of writing.

Gold, meanwhile, continues its correction, hardly surprising given its strong, speculation‑driven performance in recent years.

As for cryptocurrencies, the regime appears to have shifted. A year ago, any piece of news could send prices soaring; today, even positive developments struggle to spark interest.

Bitcoin is starting to resemble a hot potato, one investors are increasingly reluctant to hold for long. Perhaps what the market needs is, once again, an adult to step in and reignite the story.

Overall, June has brought a fair share of good news. Despite political tensions, this G7 at least succeeded in bringing the adults back to the table. Many indicators have turned positive and that’s good news for markets.

The risk, however, is that markets will now require further good news to move higher and, crucially, that negative surprises remain at bay. No easy task when valuations are near all‑time highs and investors are pushing the limits.

After all… who knows what happens when you’ve left the kids in front of the TV for too long?

)

Demystification room: Where does your money actually go when you invest?

When people talk about investing, the narrative often feels straightforward. You invest in a company, your money helps the business grow, and in return you benefit from its success. It is a compelling story, but in most cases, it is incomplete.

A simple analogy helps clarify this. Buying a stock is a bit like buying a car. If you buy it directly from the dealership, your money goes to the manufacturer. If you buy it through a platform like AutoScout, your money goes to the previous owner.

Financial markets work in a similar way. Companies only receive your money when they issue new shares, during an IPO, a capital increase or a private placement. Once those shares exist, they are traded on what is known as the secondary market, where investors buy and sell between themselves.

And this is where the vast majority of activity happens.

In practice, most of the time, when you invest, your money does not go to a company. It goes to another investor. You are not injecting new capital, but simply transferring ownership. This distinction may seem technical, but it carries important implications. If money is mostly changing hands, does it really matter? It does, because of price.

The price at which investors are willing to buy and sell a company’s shares has real-world consequences. A higher share price makes it easier for a company to raise capital in the future, to use its stock as currency for acquisitions, and to incentivize employees through stock-based compensation. It also shapes how the market perceives the company.

In that sense, market prices work a bit like real estate values. If the value of a property increases, it becomes easier to borrow against it, to use it as collateral, or to sell it under better conditions, even if no transaction has taken place recently. The same applies to companies.

This also puts the idea of “impact” into perspective. If most investments do not directly fund companies, the notion that buying a stock immediately supports a business is somewhat overstated. However, capital allocation is not neutral either. By directing demand toward certain companies rather than others, investors influence valuation and, indirectly, the conditions under which those companies can grow.

Ultimately, investing is not just about funding companies. It is about buying ownership in a system where prices are constantly shaped by other investors. Most of the time, you are not giving money to a company. You are buying a piece of it from someone else. And that is precisely why investing is less about reacting to the market and more about how you choose to position yourself within it.

SNB: Fourth hold at 0.00%... But for how long?

Article written in collaboration with PLUS, Swiss expert in accounting, taxation, insurance and mortgages.

Three months after its last decision, the Swiss National Bank (SNB) chose to maintain its policy rate at 0.00%. This announcement, the fourth consecutive pause at this level, was widely anticipated.

For property owners, future buyers and investors, this announcement extends a generally favorable financing environment. SARON mortgages remain supported by current monetary policy and fixed rates continue to evolve in relatively stable conditions.

But behind this new status quo lies a more subtle message: while the SNB isn't moving today, it's keeping all options open for tomorrow.

Discover what this quiet status quo means for your mortgages and investments…

)

)